Sorghum prices increased steadily during the year but did not have the same rally as other grains. Exports surged to record values for NSW and Australia, with crowded supply chains due to the large winter harvest sending NSW grain to ports further afield than normal, including Mackay.

cropping

Sorghum

- NSW sorghum production was the largest in a decade at 952,000 tonnes.

- Average prices in 2021-22 remained below the five-year average.

- NSW export volumes were 507,000 tonnes, double the previous year.

NSW sorghum production was the largest since 2007-08. Rain in spring that affected the winter harvest assisted the sorghum crop. While the planted area was only the largest since 2014-15, exceptional yields helped crop production to the largest level in over a decade. Early harvested sorghum was good quality, but late planted crop faced an extended harvest with rain delays.

Production

NSW Sorghum Production and Yield 201

- Production ('000 tonnes)

- Yield (tonnes/hectare, RHS)

Sorghum was planted into good soil moisture following above average winter and spring rainfall. Production increased 93% to 952,000 tonnes, while Australian production increased to 2.7 million tonnes.

201

NSW production was the highest level since 2007-08, and far exceeded the 10-year average of 477,000 tonnes.

Farmers achieved record yields of 5.6 tonnes/hectare across the state, with National Variety Trial (NVT) crops in the Liverpool Plains achieving over 9 tonnes/hectare, with one crop at Premer reaching 9.86t/ha. 25 The 10-year average yield is 3.1 tonnes/hectare. 170,000 hectares were planted to sorghum in NSW, the highest area since 2014-15, 17% above the 10-year average of 145,000 hectares.

Crops that were planted early were able to be harvested with excellent quality, but rain in April and May caused a protracted harvest and eventually reduced crop quality, with volumes of lower-grade SOR2 harvested late. 122

Price

Sorghum prices remained at elevated levels in 2021-22, having risen steadily through the year, averaging $333/tonne. This was a 2% increase over the previous year, but below the 5 year average price of $340/tonne (which included the drought years of 2018-19 and 2019-20).

Prices in NSW peaked in June 2022, with Newcastle zone sorghum reaching $375/tonne. 115 Upcountry pricing at Werris Creek had SOR1 reaching a season high of $351/tonne, and Moree reached $330/tonne. Lower quality SOR2 had a significant discount to SOR1 in December and January but narrowed to $30-$40/tonne later in the year.

Sorghum did not have the same increase in prices as other grains in early 2022 following the Russian invasion of Ukraine. Wheat and barley markets both rallied between January and June, and world wheat prices rallied in March in response to the invasion. 119

NSW sorghum was exported at an average unit value of $442/tonne, up 12% over the previous year. 35 China paid a significantly higher price for NSW sorghum than the next largest market, Japan (with a unit value of $349/tonne).

Trade

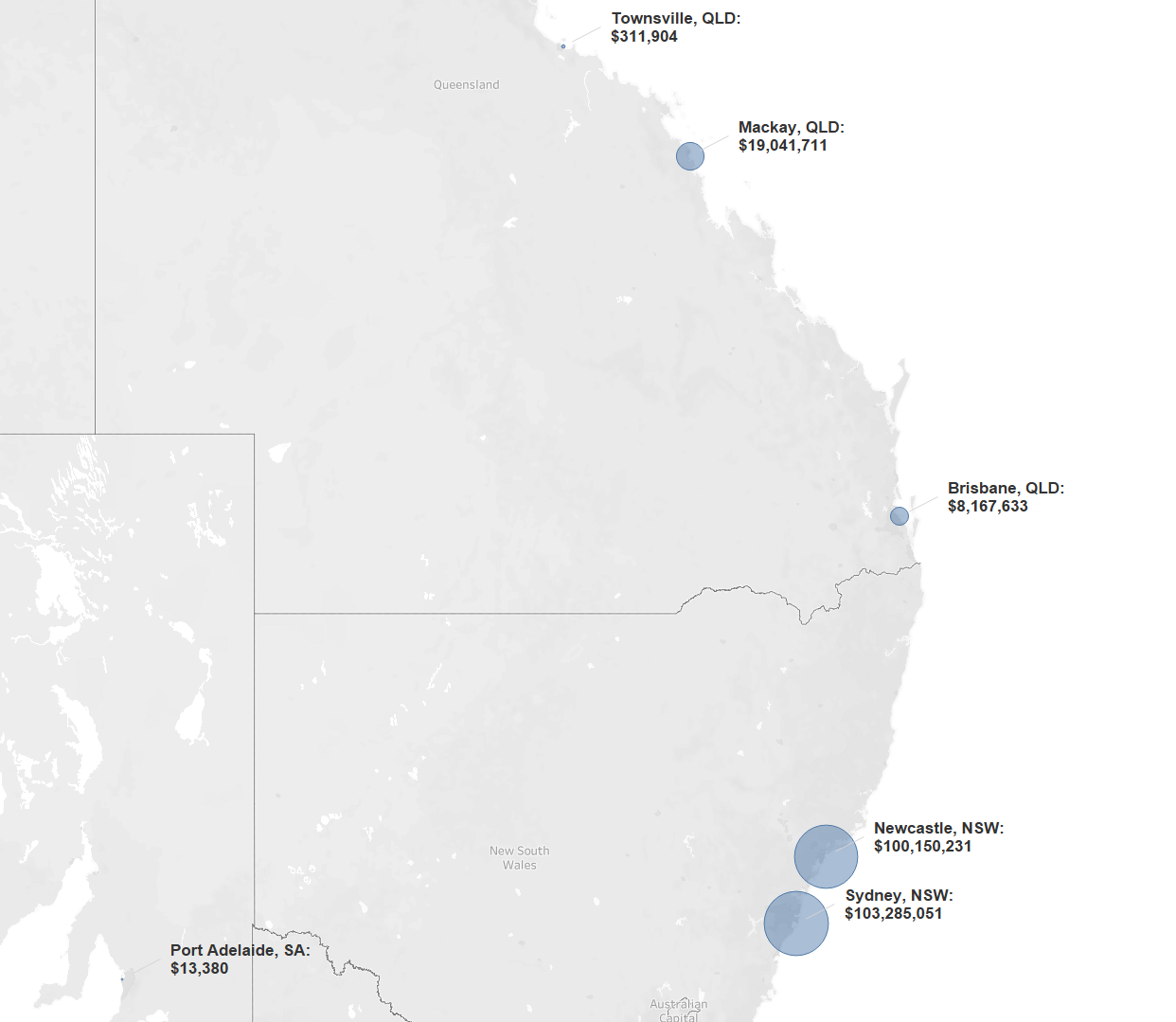

NSW Sorghum Exports by Port 2021-22

With two years of high production, sorghum exports from NSW were at record levels, totalling $231.0 million during 2021-22.

35

NSW had two months when sorghum exports exceeded the previous monthly record, with $63 million in July 2021, and $47 million in May 2022. In a sign of the exceptional year, August and June were the only months when NSW exports were not at the highest value for that month.

With consecutive seasons of high winter grain production, east coast ports were fully booked throughout the year. Exporters had to look further afield for options to get grain on vessels, and significant amounts of NSW-grown sorghum was exported through Mackay and Brisbane ports as a result.

By volume, NSW exports were more than double that in previous years, at over 507,000 tonnes. 2016-17 was the previous record at 198,705 tonnes. NSW sorghum exports were 25.0% of national exports, with Queensland accounting for 74.8%.

China remains the biggest market, with NSW sorghum exports valued at $225.4 million. Tanzania, which has not been a market for the grain previously, rose into second place with a value of $2.7 million. Exports to Philippines were $1.4 million and Taiwan was $1.2 million. Japan, which was a major buyer in 2020-21, purchased nearly all of its Australian sorghum from Queensland.

Seasonal Sorghum Exports by Month, NSW 35

- FY 2021-22

- FY 2020-21

- FY 2019-20

- FY 2018-19

- FY 2017-18

Macroeconomic Conditions

China is the world’s largest sorghum consumer, and domestic production in recent years has only accounted for around 25% of total consumption.

119

As a result China is heavily reliant on sorghum imports. The United States and Argentina are also major suppliers to China, with US production down slightly in 2022.

Most of the sorghum consumption in China is for animal feed, and the USDA estimated sorghum feed and residual use at 10 million tonnes for the 2021-22 marketing year. This reflected the recovery from African Swine Fever, with pork production in China just below pre-pandemic levels from 2018. Throughout 2021 sorghum and barley were the best value feed grains in China.

In early 2021 the Chinese Government issued new guidelines to reduce corn and soymeal use in pig and poultry feed, with sorghum included amongst the list of suitable alternatives. Sorghum usage in animal feed is much smaller than corn, where domestic consumption was 291 million tonnes in 2022. 120 However consumption of these commodities is still expected to increase in 2023, while sorghum consumption is forecast to be lower.

Outlook

NSW has benefited from this recovery in China’s pig herd with strong demand for the coarse grain.

68

USDA forecasts provide a mixed outlook with lower production and exports from the USA offset by lower imports and consumption in China.

119

However, domestically, the outlook remains positive for production with the BOM 3 month outlook showing an above 80% chance that rainfall will be above median between September and November.

117

With another full soil moisture profile at planting, ABARES has forecast sorghum plantings to be higher in 2022-23,

201

however the extended wet conditions has narrowed the planting window. While there have been some reports of difficulties securing seed of preferred varieties, overall there were higher supplies of sorghum seed.

122

Stronger Primary Industries Strategy

Grains Agronomy and Pathology Partnership (GAPP)

An innovative, multi-million-dollar partnership that combined the might of Australia’s leading research investor, the Grains Research and Development Corporation (GRDC), with the internationally recognised and applied research capability of NSW DPI was created in 2017 to drive change for grain growers.

Strategic Outcome

Economic Growth

The five-year collaborative partnership became known as the Grains Agronomy and Pathology Partnership (GAPP) with the goal to improve the yield potential of winter cereals. This was achieved by driving innovation, and building capacity and capability in strategic fields, using these three themes:

- Winter crop agronomy research covering cereals, pulses and oilseeds

- Winter crop pathology research covering cereals, pulses and oilseeds

- Capacity and infrastructure to support grains research.

The GAPP received a total investment of $64.6 million from NSW DPI and GRDC over the five years and included 58 projects undertaken at a range of trial sites across NSW.

Both parties, and importantly the grains sector, consider it a successful partnership, with the combined commitment to research collaboration reducing duplication and allowing targeted strategic research, development and extension (RD&E) projects.

The partnership between GRDC and DPI, as well as ongoing collaboration with NSW growers, has delivered immense benefit to industry through both long-term savings and returns, with growers in NSW receiving the right advice to enable them to boost their business profitability through improved on-farm cropping practices.

Some examples of the robust research put into action, where growers and advisors can use this information to make practical decisions on-farm;

- The research-based plant diagnostic service, which enables growers to identify and manage diseases early, will return $20 million to the industry over the next 10 years.

- Phenology research to create Optimal Flowering Period targets by area, which pinpoints the best cereal sowing and flowering times, will return $23 million to industry once adopted.

The five-year GAPP collaboration with GRDC concluded in 2022. NSW DPI continues to partner and co-invest with GRDC in RD&E to help growers improve their long-term profitability and sustainability.

The ongoing successful working relationship with GRDC is integral to growing stronger primary industries in NSW, with the state recording a 2020-21 cropping output of $8 billion.