Forestry

Forestry

Forestry

- Output $522m est. Steady yoy.

- Total log production up by 2% to 6.5m3.

- Bushfires in 2019-20 caused extensive damage to NSW State Forests and plantations.

Production increased in 2018-19 to 6.5 million cubic metres, but with lower prices for softwood the value of production fell 6% to $521 million.am Lower dwelling approvals and dwelling commencements in NSW and Australia likely contributed to lower unit values of softwood sawlogs, panel logs and ply & veneer logs.

Bushfires during the 2019-20 summer season caused extensive damage to NSW State Forests and plantations which will have an impact on future production.

Regrowing the forestry industry following bushfires

The NSW Government has embarked on the largest replanting program in the state’s history, beginning with an injection of $46 million into Forestry Corporation in May 2020.

Nurseries at Grafton and Blowering near Tumut will be expanded with the funding so that more than 10 million new shoots will be planted over a 12-month period across NSW after the forestry industry was devastated by an unprecedented bushfire season in 2019-20.

Koala tracking research

A koala tracking project that began in 2018 is still underway in north-east forests of NSW on the mid north-coast.

The project is using GPS collars on koalas to track their movements throughout the forest which will enable DPI researchers to look at the effectiveness of koala protections in State forests and relative use of young regenerating eucalypts after harvesting compared to mature forest that is excluded from harvesting.

Production

Total log production in NSW increased 2% to 6.5 million cubic metres in 2018-19. Softwood production was the largest component, increasing 2% year-on-year to 5.1 million cubic metres. Hardwood production also increased 3% to 1.4 million cubic metres 11.

The major categories of softwood production were sawlogs and paper pulplogs, accounting for 2.7 million and 1.5 million cubic metres respectively. Within softwoods, production increased for paper pulplogs (up 9% year-on-year), panel logs (up 31% to 345,000 cubic metres), other minor log products (up 24% to 153,000 cubic metres) and fuel logs (up 55% to 34,000 cubic metres) 11.

Hardwood production mainly consisted of sawlogs (682,000 cubic metres harvested in 2018-19) and woodchip pulplogs (502,000 cubic metres harvested in 2018-19). The value of hardwood sawlogs was steady at $100.5 million, with higher unit values offsetting a 2% fall in production 11.

Volume and value of logs harvested 2018-19

- Hardwood native

- Hardwood plantation

- Softwood

Source: ABARES (2020h)

Volume and value of logs harvested 2018-19

- Hardwood native

- Hardwood plantation

- Softwood

Source: ABARES (2020h)

Plantations

NSW had 393,200 hectares of commercial plantations as at 1 January 2019, unchanged from 2018 11. It was the second largest total area of Australia’s states and territories commercial plantations, second to Victoria’s 418,500 hectares. Softwood plantations accounted for 78% of commercial plantations at 306,000 hectares with hardwood plantation area of 87,100 hectares 11.

No new plantations were established in NSW in 2018-19 11. New plantations refer to areas not previously used for forestry. There were 9,000 hectares of replanted softwood during 2018-19 in NSW, which was the most softwood replanting in Australia 11. No hardwood area was replanted.

Radiata pine is the most common softwood species in NSW, concentrated in the Murray Valley and Central Tablelands regions, followed by Southern Pine in North Coast NSW. Blackbutt, Dunn’s white gum and other eucalypts were the major hardwood species, all concentrated in the North Coast NSW region 12.

Australia’s commercial plantation area was 1.9 million hectares in 2018-19, comprising 1 million hectares of softwood plantations, 884,000 hectares of hardwood plantations and 9,700 hectares of mixed plantations or unknown species 11.

Price

Mill-door prices in NSW and ACT averaged $122 per cubic metre for hardwoods and $68 per cubic metre for softwood products, based on a weighted average of product categories 11. Average prices had increased in 2018-19 for hardwood products but fell for softwoods.

Plantation softwood sawlogs for domestic use in NSW had a sharp decline in average prices, down 21% to $77 per cubic metre 11. This decline bucked the trend seen in other states, as average prices increased in all other Australian jurisdictions. NSW had the highest price for this product in 2017-18 but fell to the lowest average price in Australia in 2018-19. Prices for paper pulplogs in NSW increased slightly, up 6% to $48 per cubic metre in 2018-19 11.

Hardwood sawlogs for the domestic market increased slightly in 2018-19, up 2.1% to $147 per cubic metre 11. Export hardwood woodchips, the other major hardwood product in NSW, increased substantially to $90 per cubic metre 11. NSW had the highest price of all states, but the lowest volume produced.

For 2019-20, there has been diverging price trends between manufactured softwood products and hardwood products. Structural softwood timber prices fell between 1% and 3% compared to 2018-19 11. In contrast, there were higher prices in the panel products sector (which includes plywood, particleboard and MDF).

Nominal prices were also higher in many categories of structural hardwood timber. Hardwood flooring products continued its consistent price growth in 2019-20, with increases between 2% for Victorian ash and 6% for Blackbutt, compared to the previous year.

Trade

In 2019-20, NSW exports were $181.4 million, up 9% year-on-year 94. China was the largest destination, with exports valued at $158.3 million (up 12%), followed by Taiwan ($9.4 million, up 13%) and South Korea ($5.5 million, up 11%). NSW was the second largest exporter after Victoria, which exported $332.1 million 94.

Due to confidentiality issues there were $1.1 billion in forestry exports that were not attributed to any state.

By product, NSW softwood in the rough was the largest export, up 7% to $139.7 million 94. This accounted for nearly 90% of NSW forestry exports by product 94. NSW exports reached a 5-year high in May 2020 as salvage operations brought additional supply to market. NSW was a net exporter of forestry products with imports of $99.6 million in 2019-20 94.

Employment and Value Added

In 2019-20, employment in forestry and related industries in NSW was down by 7% year-on-year to 20,000 27. This was due to lower employment in wood product manufacturing and pulp, paper and converted paper product manufacturing. NSW accounted for 29% of Australian employment in the sector, which increased by 2% to 69,000 in 2019-20 27.

Industry value added (measured as production output less intermediate inputs) was estimated at $3.2 billion, an increase of 14% over the year. Industry value added for Australia was estimated at $9.7 billion, up 5% over the previous year.

Macroeconomic Conditions

Building activity in NSW was weaker in 2019-20 with the amount of activity trending lower. New house commencements were down nearly 20% in NSW and 9% across Australia 26. Total dwelling commencements were down 33% in NSW. This weakness in residential construction lead to lower demand for timber.

The US-China trade war affected the Australian forestry industry as the US imposed a tariff on paper products from China. Demand for paper fell as a result, which flowed into lower demand for woodchips. A number of shipments of woodchips from Australia to China were deferred or cancelled during the year 19, particularly from west coast Australia.

In January and early February 2020, China closed its ports over an extended Lunar New Year as part of its COVID-19 response, causing Australian timber exports to reach a 5-year low in January 2020 94. NSW timber exports appeared to be unaffected.

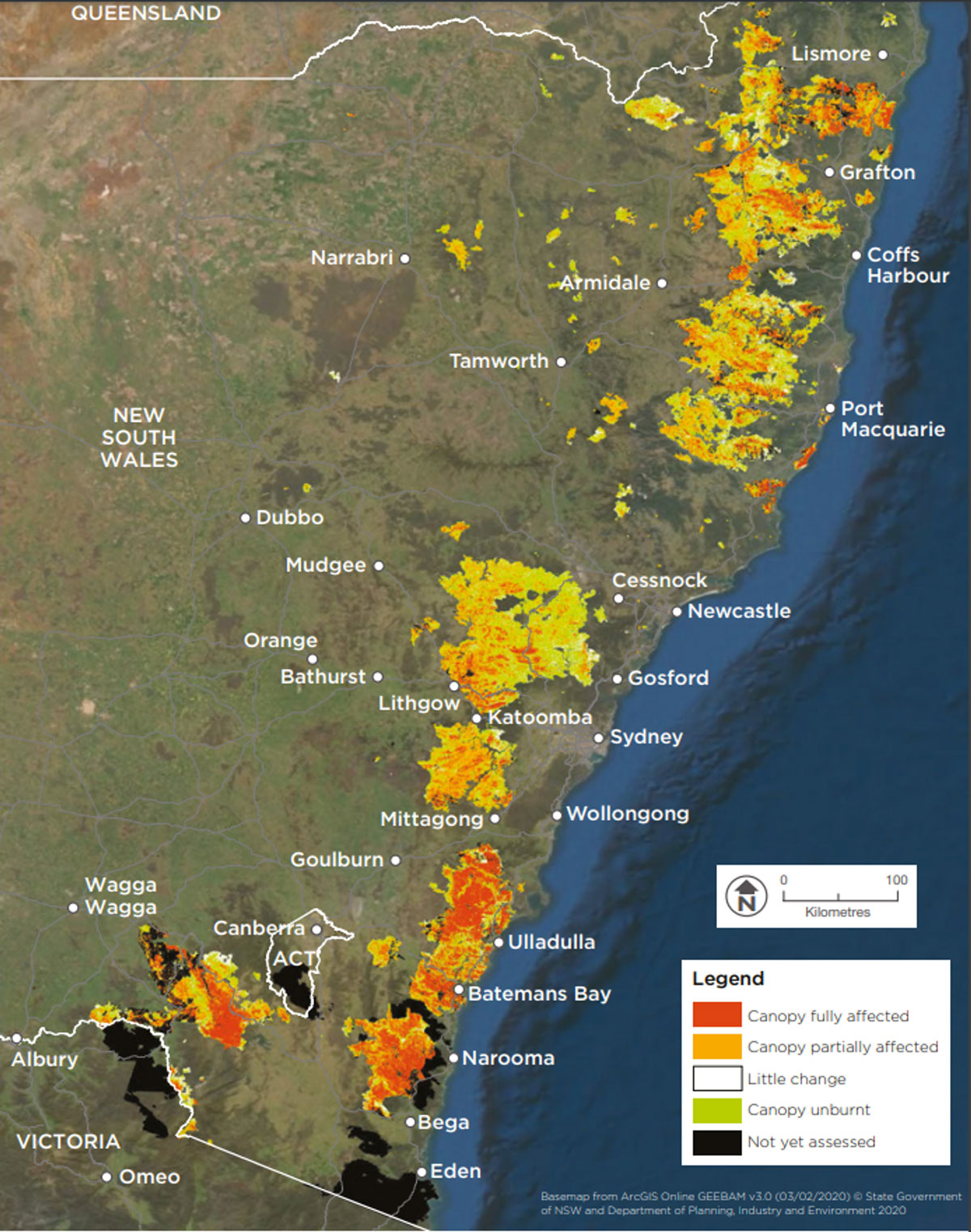

2019-20 Bushfires

The 2019-20 bushfires were some of the most devastating bushfires in the history of NSW. Over 5.4 million hectares was burnt 77, over 2,448 homes were destroyed and 25 lives were lost 116. According to the Forestry Corporation of NSW, this bushfire season impacted 890,000 hectares of native State forests and 65,000 hectares of State forest timber plantations in NSW 85.

ABARES estimated that 130,200 hectares of Australian commercial plantations were damaged in the 2019-20 bushfires, 92,100 hectares of which was in NSW 12.This represented 23.4% of the total plantations 12.

Depending on the severity of fire and the species, some commercial plantation areas may survive and mature trees in some areas could be salvage harvested. The industry is conducting salvage operations across the state to harvest bushfire-affected trees before their condition deteriorates, and mills have increased throughput in response 13.

Download pdf

10 MB