Pork

Livestock

Pork

- Output $245m est. Up 26% yoy.

- Pork prices have increased, however feed prices remained high.

- African Swine Fever impacts continued as the dominant driver of international markets.

The industry has continued to face elevated feed prices a result of the prolonged drought and substantial shifts in supply in the international pork market. Production has declined in NSW following the recent peak in 2017-18. The dominant driver remains the impact of African Swine Fever (ASF) on pork markets. China, the world's largest producer and consumer of pork has begun its herd rebuild following a 40% decline in its domestic pig herd compared to 2018 production levels.

NSW & UK join forces to protect the primary industry

DPI collaborated with the United Kingdom Department for Environment, Food and Rural Affairs (DEFRA) to build on the UK’s strategy to manage African Swine Fever (ASF) in 2020.

This provided essential information to specialised teams who make the rapid risk assessments which would be needed in an ASF biosecurity emergency.

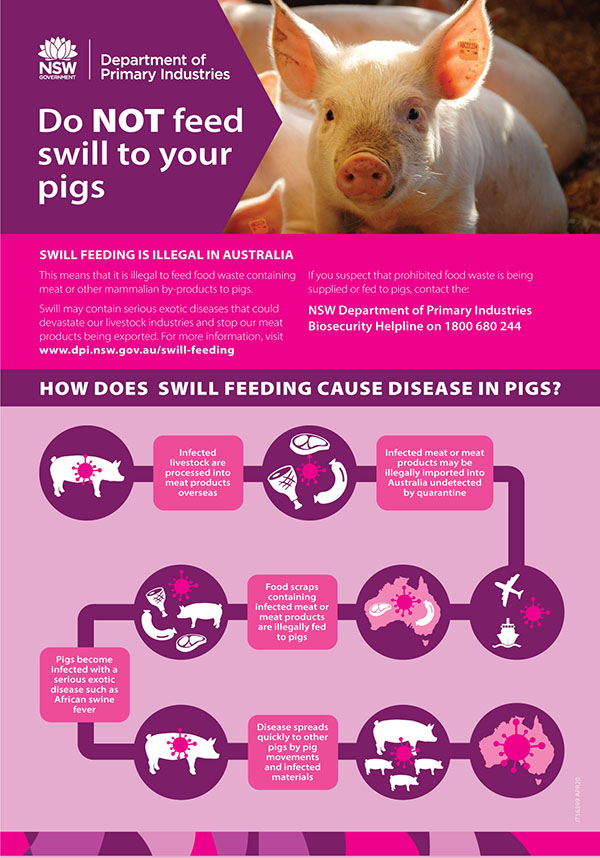

ASF has never occurred in Australia however would be devastating for pig production and health and damaging to trade and the economy.

Protecting pigs from exotic animal diseases

Good biosecurity means taking action to protect pigs from impacts of pests and diseases, including African Swine Fever (ASF).

Regardless of the size of an enterprise or hobby farm, all pig owners play a vital role in maintaining the health and welfare of livestock and providing quality pork products to consumers.

DPI offer resources containing important information about keeping pigs healthy and the biosecurity responsibilities for pig owners.

Production

Pork production has continued to decline since the recent peak in 2017-18, with a decrease of 1.3% on the previous year to 62,795 tonnes in 2019-20. Contributing to this was a 2.3% decrease in the number of pigs slaughtered to 842,000 pigs year-on-year, at the same time the average carcass weight of 74.6kg was higher by 1.0% than 2018-19 39. Underlying this trend was the size of the sow herd, a measure of the industry’s production capacity. From a breeding herd size of 57,300 sows in 2017 the herd size had decreased by 13% to 49,600 sows in 2019 24.

Pork and feed prices are key determinants of farmers’ decisions on production, with feed typically representing some 60 per cent of a pig enterprise’s gross margin costs 62. High feed grain prices were a dominant feature of the drought over the last two years. Contractions in pork production were especially marked after periods where high feed grain costs coincide with low pork prices.

While the pork industry is cyclical, the NSW herd has decreased with the total herd size on commercial farms declining from 709,500 head in 2008/09 (5-year rolling average) to 462,700 head to 2018/19 (5-year rolling average), a decrease of 35%. This compares with a decrease of 5% in the national herd over the same time 29. Reflecting continued consolidation and specialisation of pork producers, the average farm herd size has increased 98. The number of sows per farm in NSW increased to 201 sows in 2018/19 (5-year rolling average) a 45% increase over 10 years in NSW. In comparison the national average number of sows per farm increased 86% over the same period, to 298 sows/farm (5-year average) 24.

Feed grain and pork price influences on pork production

(Base year: 2000-01 =100)

- Feed price index

- Carcase price index

- Pig meat (t cw)

Source: ABS (2020b), ABARES (2019), ABARES(2020), APL (2020b)

Australian consumption of meat

- Beef and veal

- Lamb and mutton

- Pig meat

- Chicken meat

Source: ABARES (2020)

Retail prices of meat

Base: 2011-12 = 100

- Beef and Veal

- Lamb and goat

- Pork

- Poultry

- CPI

Source: ABARES (2019)

Price

Pork prices increased over the previous year with the Eastern Australia benchmark prices for porkers up 26% to an average of 410 cents per kilogram carcase weight and baconer price increasing 28% to an average of 377 cents per kilogram (cw) in 2019-20 148. The key factors influencing these prices relate to significant supply disruptions caused by ASF in China and other key pork markets and subsequently the COVID-19 pandemic.

China, the largest producer and consumer of pork internationally, suffered an estimated 40% decline in its national pig herd from the first reported outbreaks of ASF in August 2018. As a result, China accounts for an increasing portion of global pork imports to meet its supply shortfall while commencing herd rebuilding 135.

The impact of the COVID-19 pandemic also had a significant influence on the international and domestic pork industry. Most notably demand from the food services sector which accounted for a quarter of Australian pork demand. This market channel reported reductions of up to 90% for periods early in the pandemic and contributed to declining prices later in 2019-20 40.

Demand for pork by Australian consumers has been relatively constant in recent years with consumption just over 27 kg/year per capita 5. Most pork consumption is in the form of smallgoods such as bacon and ham with fresh pork consumption, supplied by domestic production is equivalent to 11.7 kg/year per capita 37. Pork meats were the second most consumed meat in Australia. A contributing factor to this demand was the relative price of pig meat compared with other red meats and in recent years pork prices have increased at or below the rate of consumer inflation 3.

Trade

Biosecurity regulations prevent imports of fresh pork meat, with processed frozen pork including middles and boneless legs typically imported to supply the bacon and ham markets. However, imports of sterile packed cooked ribs, bellies and necks also competed with domestic fresh pork 36.

The value of pork imports increased by 37% in 2019-20 with this increase being largely attributable to a 24% increase in the average unit value of imports, reflecting the higher global pork prices in 2019. The United States, Denmark and Netherlands remained the major sources for imports, accounting for 35%, 28% and 25% of the value of imports respectively 94.

At the same time exports of pork fell 23% year-on-year to a value of $23.3 million while exports in volume terms was down 31%. Higher prices for export products moderating the decline in total export values. The major export markets include Singapore, Papua New Guinea, New Zealand and Hong Kong. The Singapore represented 32% by value and 23% by volume of exports, with New Zealand and Papua New Guinea representing 15% and 11% respectively in value terms. Singapore and Hong Kong exports were generally made up of higher value cuts and carcasses while exports to the Philippines representing 15% in volume terms is made up of lower value pork products 94.

NSW pork imports, 2019-20 ($m)

- United States

- Denmark

- Netherlands

- Ireland

- Canada

- Other

Source: GTA (2020)

NSW pork exports 2019-20 ($m)

- Singapore

- New Zealand

- Phillippines

- Papua New Guinea

- Hong Kong

- Japan

- Other

Source: GTA (2020)

Macroeconomic Conditions

The Australian pork industry remained vigilant to the potential incursion of ASF. With the disease having spread through South East Asian countries including near neighbours Papua New Guinea, Indonesia and Timor Leste 38. Estimates of the potential economic impact on the Australian pork industry from widespread infection were estimated to be up to $2,033million 30. Consequently, industry and government increased preparedness including improved biosecurity measures to prevent the disease entering Australia 42.

The influence of ASF on global pork markets remains. While rebuilding of China’s sow herd has commenced during 2019-20, China’s imports remained at high levels 120. A further 57% increase in imports of pork to China is expected in 2020-21 which would support global pork prices 137.

Separately, the COVID-19 pandemic caused supply chain disruptions for the pork industry. The pandemic impacted both the supply and demand sides with lower consumer incomes and changed purchasing patterns. As an intensive industry with high throughput of livestock, it was particularly exposed to sudden supply chain shocks that can rapidly result in an over supplied market and rapid price response 119.

Download pdf

10 MB